Just a few years ago, the natural gas industry seemed to be in its death throes, nuclear power had modest comeback aspirations, and coal was king. Since then, environmental compliance costs have tossed coal under the bus, Fukishima dinged nuclear power, and fracking took off. Hydraulic fracturing, or fracking, and horizontal drilling have completely turned the natural gas industry into a runaway train. This is truly a Cinderella story of major proportions — but how long will it last? 30 years? 50 years? 100 years? What impact does this development have on our global 30-year short-term energy plan? Does it make any difference at all in the 300-year analysis? This article is a follow up analysis to a previous report on our global energy future [1]. We’ll come back to natural gas, but first let’s examine a much different story — oil.

Petroleum

What we think of as oil — crude oil from oil wells — comprises crude oil, unconventional liquids, and natural gas liquids. According to the International Energy Agency (IEA) [2], the global production of conventional crude oil peaked in 2006. Production, however, from other carbon-based liquids is on the upswing and looks to meet global demand for the near-term. But the price is also on the upswing.

The economics behind higher oil prices is clear: conventional oil has become harder to find and much more expensive to produce, which drives the need for unconventional oil — also expensive to produce. The problem is further exacerbated by the mismatch of oil characteristics (sulfur content, specific gravity) with global refining capacity and capability. The currently depressed world economy has been the primary factor limiting the price of oil. When the world economy recovers, the global demand for oil will increase, which will provide upward price pressure as supply struggles to keep up with demand. One thing is clear, we won’t return to cheap production of oil, even with a depressed world economy.

In the mid-term, say 20 to 30 years, many studies show even natural gas liquids and unconventional oil production will not satisfy demand. After that, overall oil production will begin to decline with the inexorable decline of conventional crude oil production. The 30- and 300-year projections for oil production are shown in Figures 1 and 2, respectively. As with all 30- and 300-year projections presented in this article, they are projections of the author. The 30-year projections have a 10-year basis in history and a reasonably accurate 2012 initial condition, but thereafter rely on a multitude of assumptions, and take into account, but don’t necessarily agree with U.S. Department of Energy’s (DOE) Energy Information Administration (EIA), or IEA 2035 projections. In the long term, the 300-year projections would seem to have a degree of inevitability in the endgame for non-renewable fuels.

|

| Figure 1. This 30-year oil outlook displays some IEA projections |

The 30-year oil projection (Figure 1) also includes an overlay of various IEA projections of global oil supply, for comparison purposes. For example, in 2005, IEA projected the world would produce 120 million barrels of oil per day (Mb/d) by 2030 (the equivalent of about 250 quads). For reference, a quad is one quadrillion British thermal units (Btu). A quad is also approximately 25 million tons of oil equivalent. By 2008, they had lowered this projection to 105 Mb/d, and by 2012 down another notch to a 2035 projection of 99.7 Mb/d [3]. New tight oil capacity will likely require the IEA to once again revise its projections, this time upward. However, just because oil is available doesn’t mean it will be produced. As always, economics will dominate the discussion. By 2035, the economics of oil production will likely be very different from today’s economics and production will have to take into account the economics of other energy sources.

One final note about the 2012 IEA report is that it projects the U.S. to be a net oil exporter by 2030. However, DOE EIA data show historical U.S. crude-oil imports of about 9.5 Mb/d from 2008 to 2012, with no discernible downward trend. The IEA predicts an exponential rise in U.S. tight-oil production to account for this, but has only three years of historical data for support. For the IEA projection to come to fruition, the U.S. would have to decrease its oil consumption by approximately 8–10 Mb/d by 2030 and tight oil would have to make up for the decline in U.S. conventional crude-oil production.

|

| Figure 2. The 300-year projection for oil shows a greatly decreasing output |

The 30-year global oil production (all energy liquids) is of tremendous importance and impact to the world economy in the near term. The very longterm outlook for oil, as shown in Figure 2, is bleak. The newfound shale gas and tight oil inventory may ease the decline over the next 50 to 100 years, but the longer term shows a low-output projection.

Natural gas

Anybody who, 10 years ago, predicted the resurgence of natural gas, should today be put in a class with Nostradamus. Instead of plans to build liquefied natural gas (LNG) import terminals a few years ago, the U.S. is now planning LNG export terminals. Recent technology improvements and wider use of hydraulic fracturing (fracking), along with directional drilling of shale deposits, have enabled ever-increasing natural-gas production. In the U.S. and many other parts of the world, it is a contentious environmental issue because of potential groundwater contamination by fracking fluids as well as increased greenhouse gas emissions.

Doubts linger over the longterm production capacity of these new fields because of their rapid depletion characteristics. Still, the fields are massive and even deeper fields have yet to be tapped. This newfound source of natural gas has provided low, stable costs to a resource historically known for price volatility. Low-cost natural gas has also put the brakes on plans for new coal-fired power plants, nuclear plants, and to a certain extent, renewable power. Almost all incremental new power-generation capacity in the U.S. over the last few years has been natural-gas power plants and wind farms.

Coal

Worldwide coal reserves are large, but finite, and ever more difficult to extract and transport. In the U.S., coal-based power production is surrounded by thorny political issues, including controversial mining practices, toxic air contaminants, criteria pollutants (ozone, lead, particulate matter, carbon monoxide, sulfur dioxide and nitrogen oxides) and greenhouse gas emissions [4–7]. Permitting and plans for building new coal-fired power plants have come to a near halt. Further, in efforts to refurbish 30- to 40-year-old power plants, utility companies face U.S. Environmental Protection Agency (EPA; Washington, D.C.; www.epa.gov) New Source Review action if they try to perform “repairs” without first installing state-of-the-art emission controls. Historically reliant on coal-fired generation, some electric utilities have begun accelerated plant retirement. Coal will still be important in the near-term, but increasingly less important in the longterm.

Nuclear

The March 2011 nuclear disaster in Fukushima, Japan cast a shadow over the nuclear-power industry. Most experts agree the Fukushima event negatively impacted siting and design cost for new nuclear-power-plant construction. Germany has renounced all nuclear-power production. Construction of new nuclear power plants in the U.S. is at a near standstill and seems bleaker than even the dim outlook for coal power plants. Recent retirements of the San Onofre Generating Station (2,150 MW), Kewanee Power Station (556 MW), and Crystal River Nuclear Generating Plant (860 MW) have further cast a pall on the future of the industry [8]. Recently, the president of General Electric, Jeffrey Immelt, announced he believes natural-gas power plants and renewable energy will be the best investments over the foreseeable future. This is quite a statement given that GE has its own nuclear-power-plant division called GE Hitachi. However, Asian and Russian plans for nuclear power plant construction have seen little impact from Fukushima, which counters the downward trends seen in the U.S., Europe and Japan.

Nuclear power accounts for only 7% of world energy production, and is unlikely to become a major contributor to world energy production in the next 20 years. Though proponents point to low costs and five-year plant construction schedules through introduction of small modular reactors (SMRs), even with a nuclear power renaissance, it would be difficult to justify a projection in which nuclear power would account for more than 10–15% of world energy production in the next hundred years. Estimates of uranium supply are about 100 years for the current global fleet.

Should fusion be considered a longterm solution? It still appears to be 30–50 years away from commercial viability and will require tremendous investment. In addition, it will also have to compete for economic viability with other power-producing technologies of the future. The 300-year integrated outlook in Figure 2 presents a placeholder in the amount of 100 quads beginning around 2100 for fusion and other technologies not presently viable or identified.

Renewables

The National Renewable Energy Laboratory (NREL; Golden, Colo.; www.nrel.gov) followed up its 35% renewable-power generation study with a comprehensive report making the case for 80% renewable-power penetration for the grid by 2050 [9,10]. This higher penetration rate requires grid-level energy storage, such as compressed-air energy storage, pumped hydroelectric power, large megawatt-scale batteries, or a multitude of electric vehicles [11] and additional electricity transmission infrastructure. The German coalition government goal is 35% renewable energy penetration by 2020 and 80% by 2050, the bulk to be provided by wind energy.

Less optimistic studies estimate a 10% upper-limit to wind-energy penetration [12]. However, 20% wind penetration has been demonstrated by several western U.S. utilities. In addition, a group of western U.S. utility regulators, known as the Public Utility Commissions Energy Imbalance Market (PUC EIM), seeks to develop large consolidated energy balance areas for the purpose of lowering consumer-electricity costs and increasing grid reliability through use of renewable-power production.

The renewables cost question is a particularly complex issue. Renewable-energy proponents often cite low-levelized cost of energy (LCOE) for wind relative to nuclear, advanced coal and natural-gas peaking turbines, and roughly equivalent costs when compared with combined-cycle natural-gas plants (depending whether the U.S. production tax credit is factored in or not). Opponents point out that this doesn’t account for backup power sources that are required to account for wind’s intermittent nature and dispatchability issues. The answer likely lies in the future nature of the electricity grid, which will be quite different from today’s grid. Grid-wide visualization tools such as phasor-measurement units (PMUs), large balancing areas, high-voltage, direct-current (HVDC) transmission lines and converters, and a major injection of energy storage over the next century could provide the means for renewables penetration.

Water — energy’s hidden cost

Water has become an endangered resource in critical settings, especially freshwater drawdown that competes with agricultural and urban use, in Texas, for example [13]. Many aquifers serving major cities have recorded increasing depletion rates. Water use will be a cost that cannot be ignored. A recent study of electricity costs (risks, subsidies, water and environmental) [14] presents water usage requirements of extraction and power production. For instance, water used for hydraulic fracturing is typically estimated to be two to eight million gallons per well. Coal production, as well, can be water-intensive relative to extraction.

Power production, whether via combustion or nuclear, creates waste heat — lots of it. Almost two-thirds of coal, nuclear, natural gas, and biomass plants use closed-loop cooling systems, which lose 200–1,000 gal/MWh of water through evaporation [15, 16]. The remaining one-third of these plants use open-loop systems, which lose even more water. In contrast, water impacts from solar and wind plants during operation are almost negligible. Electric Power Research Institute (EPRI) estimates a cost of about $100 billion for U.S. power plants to comply with U.S. Clean Water Act for closed-cycle cooling retrofits [17].

The integrated picture

|

| Figure 3. This 30-year integrated global energy plan shows natural gas and renewables coming to the forefront |

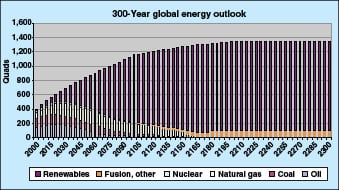

|

| Figure 4. The 300-year outlook for energy production shows a massive increase in renewables |

The 30-year plan. Figure 3 shows the integrated global energy picture over the near-term of 30 years. It was derived using a top-down global energy projection reconciled with bottoms-up individual energy source projections. A more optimistic energy-use projection could result if the global economy picks up and energy sources become less expensive to produce. A less-optimistic projection could result if the global economy remains depressed and wholesale energy conservation measures are adopted.

Non-renewable energy resources, such as nuclear, oil and coal, appear stable over the next 30 years, but won’t contribute to satisfying the increasing global energy demand. Natural gas and renewable resources, however, appear poised to do the heavy lifting.

The 300-year outlook. Figure 4 shows the general trends of energy production for the next 300 years. Over the next three centuries, the burning of fossil fuels for electricity generation is projected to decline, even as the overall energy demand increases. The percentage of energy attributable to renewable sources will increase as fossil fuel reserves are depleted and renewable technologies mature.

The longterm plan

One potential play would be to combine natural gas and renewables to replace coal and oil in the next 50 to 100 years. This type of hybrid plant has been demonstrated extensively with large-scale solar at the Solar Energy Generating Systems, or SEGS, near Kramer Junction, Calif. Hybrid facilities serve to firm the non-dispatchable, intermittent nature of pure renewables such as wind and solar. This would reduce carbon dioxode emissions, while acting as an interim step to 100% renewables.

Some may deny the possibility of a 100% renewables scenario in as little as 300 years, or ever. Yet, our non-renewable fuels are just that — non-renewable. From a chemical engineering perspective, would it not be more appropriate to use fossil fuels as feedstocks for chemicals, plastics and other recyclable products rather than burning them for fuel?

“We are like tenant farmers chopping down the fence around our house for fuel when we should be using Nature’s inexhaustible sources of energy—sun, wind, and tide. I’d put my money on the sun and solar energy. What a source of power! I hope we don’t have to wait until oil and coal run out before we tackle that.” — Thomas Edison, 1931.

References

1. Botsford, C., Global Energy Future: The 300-year Outlook, Chem. Eng., Jan. 2012. [Read online]

2. International Energy Agency World Energy Outlook (2009). [Read online]

3. International Energy Agency World Energy Outlook (2012). [Read online]

4. Energy Information Agency, U.S. Dept. of Energy. [Internet] 2011. [Read online]

5. Energy Information Agency, U.S. Dept. of Energy. [Internet] 2011. [Read online]

6. Electricity – Significant Changes are Expected in Coal-Fueled Generation, but Coal is Likely to Remain a Key Fuel Source. US GAO, Oct. 2012. [Read online]

7. Johnson, K., Plan to Curb New Coal Plants, The Wall Street Journal, Sept. 12, 2013.

8. Energy Information Administration, U.S. Dept. of Energy. [Internet] July 2, 2013. [Read online]

9. Lew, D. et al., Western Wind and Solar Integration Study, National Renewable Energy Laboratory (NREL), Dec. 2010.

10. NREL Analyses; Golden, Colo.; www.nrel.gov. [Read online]

11. Jenkins, S., Transporting Energy Through Time, Chem Eng., Dec. 2011. [Read online]

12. Korchinski, W. The Limits of Wind Power, Oct. 2012.

13. Grubert, E., F. Beach, M. Webber, Can Switching Fuels Save Water?, iopScience, 2012. [Read online]

14. Keith, G., S. Jackson, A. Napoleon, T. Comings, and J. Ramey, The Hidden Costs of Electricity, Sept. 2012. [Read online]

15. Energy Information Administration, U.S. Dept. of Energy. Nov. 17, 2011. [Read online]

16. Wagman, D., Water Issues Challenge Power Generators, POWER, July 2013. [Read online]

17. Bailey, D., Potential Impacts of Closed-Cycle Cooling Retrofits at US Power Plants, POWER, Nov. 2012. [Read online]

Author

Charles Botsford, P.E. is a professional chemical engineer (Email: botschas@gmail.com) in California with 30 years experience in engineering process design, distributed generation, and environmental management. He has a wide range of experience relative to oil refining, power electronics, renewable energy systems, electric vehicles, and air-quality issues. Botsford is a Qualified Environmental Professional (QEP) Emeritus. He holds a B.S.Ch.E. from the University of New Mexico, and a M.S.Ch.E. from the University of Arizona.

Charles Botsford, P.E. is a professional chemical engineer (Email: botschas@gmail.com) in California with 30 years experience in engineering process design, distributed generation, and environmental management. He has a wide range of experience relative to oil refining, power electronics, renewable energy systems, electric vehicles, and air-quality issues. Botsford is a Qualified Environmental Professional (QEP) Emeritus. He holds a B.S.Ch.E. from the University of New Mexico, and a M.S.Ch.E. from the University of Arizona.